The Rise of the MSO

What Lawyers Can Learn from Doctors

I believe that the legal profession is going to change dramatically over the next few years. At Edge, we are already seeing this with our existing customers. We are often asked to give advice on what we see and where we think the world is going. So, this is the first of a series on how AI will affect the legal profession.

The first post in this series is about the rise of the MSO, or Managed Service Organization. What is an MSO? It is an operating company owned at least in part by non-professional capital. It purchases equipment and software in bulk, negotiates leases, employs administrative staff, and more. Because it is technically not a professional practice, it can also raise equity capital and is typically easier to underwrite for debt by creditors. In exchange for all it does, although the MSO typically does not directly own shares in the professional practice, it extracts fees—often 90%+—that equal de facto ownership.

Lawyers are just starting to hear about them. What are they, and why are they emerging now? In this post, I argue that the future law firm will increasingly use MSOs and that there is much to learn from the medical field, which pioneered the use of MSOs in a profession.

The Rise of Medical Capital

Historically, physicians were small business owners. But now things are increasingly consolidating. At the same time, the medical profession has boomed, and medical spending is now nearly 20% of GDP. Why? And are these related?

The story you’ll hear in the press is about private equity driving up prices and pushing consolidation, but I believe the story of this capital flow is typically told backwards, however, confusing cause and effect. Usually, the story is that the rules got loosened, capital flowed in, and this changed the medical profession. But I believe it was inevitable because of the changes in the practice of medicine. To understand why, let’s look at the history of medicine in the United States.

After World War II, the United States embarked on a journey of heavy scientific research, especially in medicine, with the institution of the NIH and NSF, alongside specific efforts like President Richard Nixon’s war on cancer. The result was the rise of specialty care and increased capital costs as medicine got more sophisticated. You were naturally going to require more capital to fund this specialization and technology.

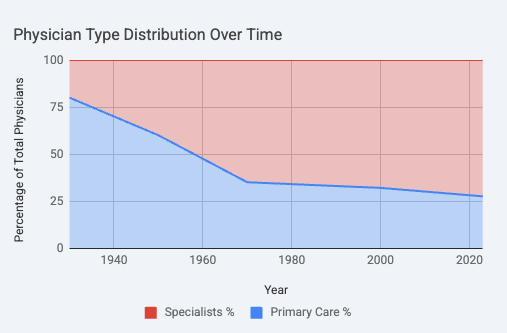

Still, the Normal Rockwell image of the home doctor is what most people would have experienced before our medical revolution. This changed rapidly, and you can see it in the data.

Even after the standardization of the medical industry after the transformational Flexner Report in 1910, in 1931 84% of doctors were still general practitioners; by 1965, only 37% were. In 1931, there were 17 specialties; today, there are 40 specialties and 89 subspecialties. This brought up the capital costs needed to start a practice as well as the operational complexity needed to practice medicine.

With specialization, suddenly it wasn’t enough to have a community, an office, and a stethoscope to practice medicine. You needed to work with complex insurance schemes, you needed more specialized space, and you needed to spend possibly millions of dollars on specialized equipment just to practice your area of medicine.

Increasing complexity is usually dealt with through economies of scale. Larger organizations are able to spread out operational costs and complexities through a larger revenue base. And so it was in medicine: increased specialization drove consolidation.

The problem is that while medical training in the US is the best in the world, meaning that most doctors are good at their jobs, they are often not businesspeople. That means that in our hyper digital world, they are bad at marketing themselves, bad at business operations, and just often bad at the things you need to do to run a business.

This naturally attracts capital to the medical business, as it would any business field.

While what you may have in mind is the growth of private enterprises, like HCA, and giant hospital systems that seem larger than ever (note how many states have a hospital as its largest employer), the other main effect has been physicians buying each others’ practices. Taking on capital partners, business-savvy doctors are buying other practices 5-10 at a time and creating mini local empires of practices. This has also allowed them to bring in operating and technology partners.

The problem is that all of this is very, very expensive. Thus was the rise of the MSO: it was a response not to scale but to a need for capital.

While a few states, like New York and New Jersey, are still relatively restrictive on practice ownership, most states like California only require majority 51% ownership by physicians. Some states, like Florida and Illinois, have no such restrictions at all. And everywhere, this restriction is skirted through MSOs. This change began in 1982 as a result of the famous case American Medical Assn. v. FTC, 455 U.S. 676 (1982), where the FTC won a victory against the AMA for restricting non-physicians from any involvement in their practice.1 And while fee sharing is heavily regulated under the Anti-Kickback Statute and Stark Law, fee splitting is looser in medicine than in the law.2

Today private equity owns 30% market share in at least one specialty in 31% of all US metropolitan areas. This arrangement all works through MSOs.

What’s Next for Law Firms?

You’re already seeing things change. Arizona and Utah were the first. Soon Texas will be next. The dam is about to break on so-called sandboxes.

This sounds like the story we saw before with medicine, but there is a very key difference. Lawyers are extremely strict about sharing the money with nonlawyers, even aside from kickback concerns. Ethics rules prevent any fee sharing with non-lawyers, even referral fees, under ABA Model Rule 5.4, which most jurisdictions follow. Similarly, they do not allow for even a quantum of non-lawyer ownership under independence rules. These rules have restricted access to capital and business model innovation. In contrast, medicine has been able to allow massive flows of much-needed capital to enter the healthcare industry as a result of better-configured rules.

AI is going to change the economics of the law practice. It will drive profitability and increase revenue, but it will also change some of the required skills and training practices, increase the operating costs of running a law firm, and increase the returns to business savviness. Think of it as raising the barrier to entry, increasing the returns to scale and modernization, and ultimately rewarding law firms that are better run from a business perspective.

The legal profession underwent a change in specialization during the same period as the medical profession did. I would actually go further and say that the legal field is 100% specialized today; I wouldn’t even know what to call a “general” lawyer. There are IP lawyers, personal injury lawyers, employment lawyers, tax lawyers, criminal defense lawyers, trust and estate lawyers, securities lawyers, and much more. Even “corporate lawyers” only handle a subset of corporate law.

And yet firms have gotten much larger without requiring outside capital. Why? The reason is that the law is abstract so increasing specialization did not require increased operational complexity or capital requirements. A great litigation partner does not require a more expensive Lexis Nexis subscription than the next person, while a neurosurgeon will require ten million dollars of equipment to even start doing their work that is different than the ten million dollars of equipment required by an oncologist. Although the value of brand and economies of scale for administrative tasks justifies consolidation, it does not require outside capital in and of itself, and thus no MSO was necessary, and the legal profession remains more fragmented than the medical profession. With AI, this is no longer true. Extraordinarily expensive software, specialized per practice, is becoming the norm. AI is the equivalent of medical equipment for lawyers.

This is going to drive much more M&A, as we’ve already seen in the news. But it won’t just be big firms. Many larger boutiques are going to want to merge—who wants to be two 50-lawyer firms with a narrow focus when you can be one 100-lawyer firm that is full-service in your niche? MSOs will be a key part of this, not only because they will make it easier for firms to partner as collectives but more importantly because it will allow law firms to access capital and talent. Take Crosby, a new-age law firm. Because they have an MSO, they can offer stock options to the best technical talent in the world and raise venture capital, which they did from Sequoia, one of the world’s leading venture capital firms. Notably, McDermott Will & Schulte LLP, number 23 of the Am Law, is now considering an MSO specifically for the purpose of bringing in private equity—after all, they just bought Schulte Roth & Zabel LLP. Neither of these firms will be the last.

I do believe, as well, that this will also allow for an increase in collaboration between law firms and technology companies. Why is there no ZipRecruiter for law firms? Because ZipRecruiter could not charge a fee, which destroys the market for both sides—that’s fee splitting for the lawyers and the elimination of the incentive for ZipRecruiter. I believe that many technology companies are forced into an unnatural arrangement where they are forced to try and sell software to lawyers due to this rule. There are many businesses that would be better off as a marketplace charging a fee, or charging tied to completed work, or as a top-of-funnel referral network. All of these would fall afoul of Rule 5.4 but are acceptable with MSOs. In other words, the MSO should also allow for more experimentation in business models, which the law sorely needs.

Conclusion

So where does this leave law firms?

The legal industry is currently where medicine was in the 1970s: highly fragmented, resistant to outside capital, and clinging to a “craftsman” identity even as it has scaled significantly. But as the “scientific revolution” of AI raises the cost of entry and the complexity of operations, the lone practitioner will become as rare as the 1930s GP.

The future of law isn’t just “more computers.” It’s a fundamental restructuring of who owns the firm, who shares the profits, and how legal expertise is delivered at scale. It will leave the legal professional more efficient and better run.

Curiously, the FTC’s lawyers never decided to pursue the same action against the ABA.

It is curious that kickback statutes do not apply to law firms, but it is even curiouser that they do not obviate the need for limitations on professional ownership or fee splitting. The main public justification for keeping professional businesses within the profession is to avoid clouding one’s professional judgement, but it is not obvious why unscrupulous billing practices are less so when the incentive-warping party is merely of the same profession. What matters is the presumption of good judgment in a dispute and the nature of the decision made. In a sensible world, perhaps all such “in the family” rules are replaced with strict kickback and professional judgment rules.