Study: How IP Can Help Your Startup

Plus! Nokia launches a 5G patent war, a key GPU cacheing patent application, and a new Saudi initiative with Singapore

Should startups get patents? With an early stage company, time and money are in very short supply, and a patent can require quite a bit of both to successfully obtain. In fact, the advice that many companies get—including at Y Combinator, the world’s top startup accelerator in which the patent assistant Edge participated—is to avoid getting a patent unless your industry, like biotech, requires it. This advice tends to follow the reasoning mentioned above, but is short on something important: data.

The European Patent Office (“EPO”) has come to the table with a new paper answering that question using data, not anecdote. The result is contrary to the conventional wisdom: companies with intellectual property are more likely to raise venture capital and more likely to exit at higher values. And not by a little: startups are more than 6 times more likely to raise an institutional round and more than 3 times as likely to IPO. And although this paper focuses on the EU, other research has found a similar effect in the United States, including data showing that patents reduce the time to VC financing by 76% and increase sales by 79.5% over 5 years.

In this week’s Nonobvious, we will go deep into this paper to give you the numbers and help explain how intellectual property actually can help in the startup journey.

The IP Boost in the Arm

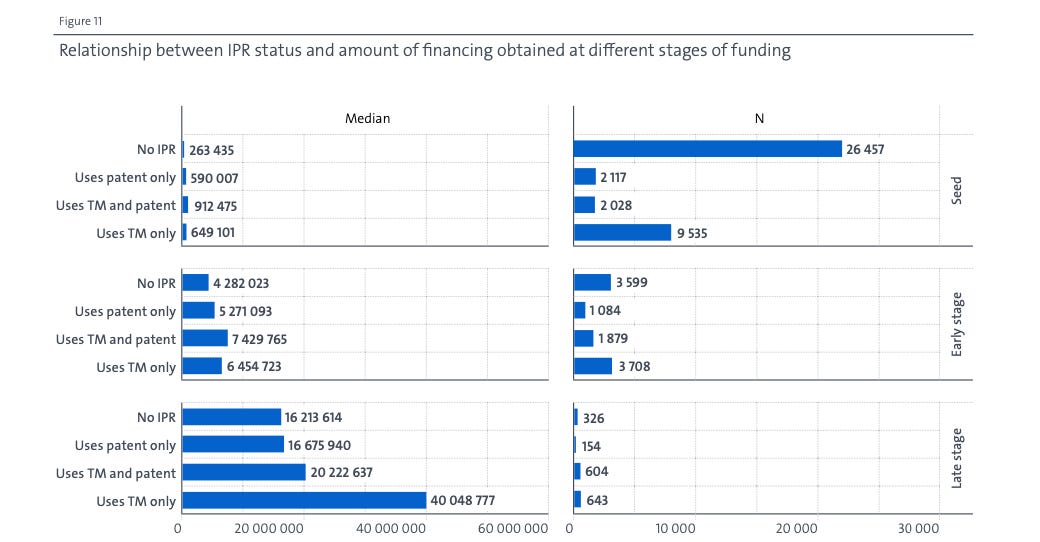

There are two big takeaways from the study. The first is that patents make startups much more likely to raise venture capital, and interestingly they make a bigger difference at the Series A stage rather than the seed stage. In fact, of startups that have filed by IP at the seed stage, 28% applied for trademarks while only 10% applied for patents, which nearly triples to 29% applying for patents at the early institutional stages.1 Similarly, having a patent has a bigger impact on raising a round at the early institutional stage than the seed stage: a startup with a patent is 2.9 times likelier to raise a seed round, but 6.4 times likelier to raise an early institutional round. The other major finding is that obtaining IP has a major impact on getting an exit. Companies with patents are 2.1 times more likely to get acquired and 3.5 times more likely to IPO. These are large numbers and a much bigger boost than trademarks. Notably, patents also have an impact on exit values.2 Companies with patents have a 3.2 times higher acquisition value and a 2.4 times higher IPO value than companies without them.3

Why does this occur? There are likely a few reasons. If you ask companies themselves, a survey found that the top reasons companies believe their IP is valuable is generating revenue and defensive use. The EPO also observes that there is a significant literature indicating that IP also serves a signaling function: that is, if your company has its act together enough to file for IP and have a coherent strategy, that likely says something about other unobservable factors. Signaling likely also likely helps explain why European patent applications4 provide a bigger boost than national patents at every stage of the analysis. This is likely in part due to signaling too, since it implies a bigger ambition. But in our view, the EPO underplays the explanatory power of the hard benefits of patents. A European application has broader potential protection than a national patent, allowing the startup to target a bigger market. And IP represents an asset that can be licensed for additional cash flow or sold in the event of bankruptcy. The first allows startups to boost their cash flow in a non dilutive fashion while the second provides risk protection, which startups often lack. That said, though the study offers many guesses as to the causal mechanisms, the data isn’t rich enough to prove any of them.

As is to be expected, there are significant differences in the IP patterns of startups by industry. Biotech has the most patents, and some of the usual suspects in heavy industry have high patent rates as well, like energy, manufacturing, and consumer electronics. But some surprising industries have high patent rates, like artificial intelligence, navigation and mapping, and health care. Trademark use is relatively uniform, though the variation is also roughly correlated with patenting rates.5 Although there is some difference in the importance of IP by industry, like in biotech (where patents are essential), the effect appears to be consistent across industries, and in any case they control for the industry effects; in other words, the effect is true even accounting, for example, for the overrepresentation of IP-sensitive industries in the sample.

The EPO study has some limitations in the data. First, it divides startups into seed stage, “early stage” (Series A and B), and “late stage” (Series C and up). Although this is a reasonable approximation, these days the name of a round is not a perfect proxy for the stage of development of the company. Furthermore, the data comes from Crunchbase, which is less accurate than more proprietary databases like Pitchbook and CB Insights. Furthermore, Crunchbase’s data on funding round size is the least accurate part of its data set. That means that there are certain questions that couldn’t be answered—for example, do patents help companies secure bigger rounds? Certain other questions, like whether IP helps companies attract higher-quality investors, are also left unanswered, perhaps in part to avoid making a determination of which investors are better. And, of course, the EPO only studied European startups, not the broader ecosystem, so there may be differences in other regions of the world not covered by this study.6 And most importantly, because many of these companies have private financials, the study authors are unable to measure the impact of patents on revenues, especially for companies that become successful but stay private.

Of course, whether a startup pursues IP will be up to their specific circumstances—whether their innovations are patentable, the availability of funds, their counsel’s assessment of the tradeoff of disclosure against confidentiality, and more. But the data does show that patents are more valuable than is typically believed, even for startups, and founders should take this into consideration when making strategic decisions.

Weekly Novelties

Gripping Gazette entries

US 11,738,875 B2: A hybrid propulsion system for aircraft to help advance the dream of electric-powered flight

US 20210271606 A1: An application for dynamic GPU cacheing from Apple, which appeared in a product for the first time this Halloween with the launch of the M3 processor

US 11,801,329 B2: A patent for a plant-based dermal filler that enables tissue regeneration

Latter-day litigation

Nokia Technologies OY v. Amazon.com Inc, U.S. District Court for the District of Delaware, No. 1:23-cv-01236: A massive case from Nokia against Amazon over 5G patents. Nokia has said it has over 20,000 patents, so there’s more where that came from, including simultaneously filed cases in multiple countries and an identical suite of cases against HP

Malvern Panalytical, Inc. v. TA Instruments-Waters, LLC et al, No. 22-1439 (Fed. Cir. 2023): A presidential claim construction decision, mainly saying that you cannot rely too much on just reading an IDS statement to override a commonly-understood definition without explicitly differentiating in the specification

Gamevice Inc. v. Nintendo Co. Ltd., U.S. District Court for the Northern District of California, No. 3:18-cv-01942: Nintendo wins a lawsuit on a summary judgment on the design of its controllers; the Switch has been the subject of many lawsuits but Nintendo keeps coming out on top

Eventful expirations

US 6637036 B2: Protective hockey pants, probably just as essential for the sport as ski pants are for theirs

US 6637046 B2: A cover for pools and hot tubs that use a technique similar to corrugated paper to more efficiently protect heat

US 6637063 B1: A sensor for automatically assigning a bridge to an aircraft in an airport; it would be bad if this was ever messed up!

Notable news items

An analysis of AI patent applications: unsurprisingly, they fell off after Alice v. CLS Bank and have increased in recent years since, but surprisingly the allowance rates are quite high (Mintz)

Saudi Arabia, in a bid to shore up its tech center bona fides, announces a joint patent program with Singapore (Lexology)

As the consumer electronics patent wars continue, a potential injunction against Apple Watches before the holiday season raises questions about the right policy, again (New York Times)

The EPO guesses that this is primarily due to the technology being in its infancy, but a more likely reason is simply that trademarks are much cheaper, so it is difficult to file for a patent before receiving more institutional money.

Oddly, despite estimating that companies with IP exit at higher values, they do not also estimate whether this effect is the same for venture capital. This is likely due to data quality. Exit values are reported more often and accurately than valuations or dilution numbers.

That said, the EPO notes that exit valuation data is spottier. With IPOs, in particular, the EPO is relying on Crunchbase, but given that these are crowdsourced numbers, it is unclear that all contributors are using the same definition. With an acquisition, the exit value is relatively straightforward to report, but with an IPO one must be careful to be consistent—is it the IPO price? The first day closing price? Some 30 day moving average?

Note that here that while the EPO refers to “European patents” through the paper it is not talking about a European Unity Patent, which is a new innovation from 2023 that did not exist for most of the sample. They are using this as a shorthand for patent applications.

This introduces questions of autocorrelation in the Cox Proportional Hazard econometric model, which they do not describe accounting for.

This is a slightly puzzling choice, given that the EPO’s search tool, Espacenet, covers over 140 million patents across over a dozen key jurisdictions, from the United States and Japan. Also surprisingly, even within the EU, the study doesn’t control for differences across countries despite the fact that they have the data.